Titanic Syndrome: Why Companies Sink and How to Reinvent Your Way Out of Any Business Disaster

The fast-moving up-and-down economy we live in makes keeping our companies afloat increasingly difficult. Just as we handle one crisis, another appears.

Digital, millennials, new regulations, new competition, political turmoil, Artificial Intelligence, Industry 4.0, Blockchain, sharing economy, circular economy, substitute products, you name it — the waves of disruption come crashing faster and faster, fundamentally changing the way we work, profit, and compete.

For nearly 20 years, I’ve worked in the field of survival and sustainability — researching and developing ways for businesses to stay afloat, no matter what the disruption. To understand the mechanics of survival, it helps to look at the successes and failures of the past.

One of the most illustrative failures of all time: The Titanic. In fact, its story offers eerie parallels between the behavior of the ship’s team and that of teams in today’s at-risk companies.

On a chilly Sunday, April 14, 1912, at 11:49 pm, the Royal Mail Steamer Titanic — en route from Europe to New York City — collided with an iceberg and sank within three hours, leading to the deaths of 1,514 of the 2,224 passengers and crew onboard.

The largest moving man-made object at the time[i], the Titanic was considered unsinkable by all: experts, media, and the public. The ship was equipped with the most advanced naval technology available, as well as a crew of experienced and respected naval leaders.

What is the Titanic Syndrome?

Titanic Syndrome is an organizational condition where companies ignore internal problems, resist change, and continue harmful behaviors despite warning signs. Named after the Titanic disaster, it describes businesses that fail to adapt, leading to decline or collapse due to overconfidence, denial, or poor leadership.

So why did it sink (and what can we learn)?

What killed the Titanic?

Death Factor #1: Ignored Warnings

Most of us know that the Titanic’s crew was warned about the area’s dangerous icebergs. But how many times were they warned? At least six!!! The last and most specific of the six was not passed along to the captain because the radio operator interpreted the message as non-urgent, and returned to sending passenger messages to the receiver on shore at Cape Race, Newfoundland before it went out of range.

The radio operating team was so concerned with keeping the high-paying customers — 1st class passengers — satisfied, that they told the passing ship Californian, “ Shut up, shut up, I am busy; I am working Cape Race[ii]”, when interrupted on-air by his counterpart warning of the upcoming ice field.

Customer satisfaction is all the rage. But killing it for the wrong whim of the customer might accidentally kill your business.

Death Factor #2: Over-Reliance on Past Success

On the night of the collision, the captain had already gone to bed. First officer William Murdoch was in charge. At 39, Murdoch had 16 years of maritime experience and was known for his masterful record of averting ship collisions.

For instance, prior to the Titanic, he had served on the Arabic, when a passing ship came bearing down from out of the darkness. Murdock overrode his superior’s command, and instead rushed into the wheelhouse, pushed the quartermaster aside, grabbed the wheel and held the ship steady. As a result, the two ships passed within inches without damage[iii].

The Arabic incident was one of many Murdoch mastered in his career. In the 37 seconds between the first sighting of the iceberg and its collision with the Titanic, the officer fully relied on his past successes to make executive decisions in the present. We all know how that turned out.

What got you here won’t get you there. Instead, your own previous success might actually destroy your every dream.

Death Factor #3: No Binoculars

The night of the collision was clear and still. Perched 50 feet (15 meters) above the forecastle deck, in a small open box called “the crow’s nest,” lookouts Frederick Fleet and Reginald Lee worked their two-hour shift. Inside the nest, Fleet and Lee had a large bell to grab general attention and a telephone to reach the captain’s bridge. What they did not have, however, was a pair of binoculars.

A hundred years later, with all the advances in modern technology, it is still hard to imagine any ship in the open waters with no binoculars. The Titanic, too, had a number of binoculars on board, but for much of the trip they were in a storage cabinet, locked up.

The key to the cabinet was held by Second Officer David Blair, who, in a last-minute leadership change decision, was asked to sit out the trip before the ship’s departure from Southampton[iv]. Leaving the Titanic in haste, Blair forgot to hand the key to his replacement. It is likely that the cabinet or its lock could be broken. However, nobody made the call.

Frederick Fleet, who survived the disaster, would later insist that if binoculars had been available, the iceberg would have been spotted in enough time to take evasive action[v].

By the time the iceberg was noticed, the ship was too close to avert disaster.

This was, quite literally, a case of overconfidence that was blinding.

The Role of the Iceberg

We’ve already reviewed a number of the disaster’s causes, but we seem to have missed the main one: the iceberg. Whenever we work with a company or discuss the Titanic story on stage, the iceberg is among the first causes mentioned.

Most of the time when we are asked to work with a company on reinventing their products, processes or the entire business model, we are not there during the good times. By the time we are called, things are already deteriorating — the iceberg has been hit, so to speak. And oh boy is it easy to blame the iceberg!

Sneaky competitors, overbearing regulators, bad weather, bad design, late suppliers, lazy customers, those finance-department knuckleheads: we heard it all. It is so easy to blame it on someone else.

But here is the thing: while you cannot prevent the iceberg from appearing, you can darn well make sure you don’t hit it. The choice is in your hands.

Titanics of the 21stCentury

We already talked about several problems that helped sink the Titanic, but there were others. The quality of the ship’s metal was questionable. The construction was rushed. Even after repeated warnings, the ship was traveling at a dangerous speed. Onboard, there were no red flares, so the crew of a passing ship mistook the Titanic’s panicked white flares for festive fireworks.

But of all the things that went wrong, there was one problem more important than the others: the arrogance and overconfidence in past success.

Embedded in every aspect of the Titanic’s operations was the assumption of the ship’s mighty power. In the eyes of all involved, it was unbreakable and unsinkable. The team became over-confident and complaisant. The unsinkable lead to the unthinkable.

The Titanic story is known throughout the world, so it’s hard to imagine that it could repeat itself. Yet, every year with remarkable consistency we see companies large and small calling SOS, amidst a business crisis. Many of these companies end up getting acquired, declaring bankruptcy, or even worse — never recovering. One statistic best illustrates the poor survival rate of the business world’s “unsinkable titans”: of the 500 mighty companies originally included on the Fortune 500 in 1955, today only 60 survive. That’s a sinking rate of 88%.

Take, for example, the best known ‘Titanics’ of the 21st century: Kodak and Nokia. Kodak had been the staple of American culture throughout the 20th century, selling at one point 90% of all photographic film and 85% of all cameras in the United States. Nokia had been the number one cell phone seller from 1998 to 2007, controlling at its prime 40% of the entire global handset market. Yet, Kodak filed for bankruptcy in 2012, while Nokia was forced to sell its mobile device business to Microsoft in 2013 to save itself from collapse.

The story of the Titanic is the most powerful example of a “too big to fail” mindset. Our friends at Kodak and Nokia suffered from the same disease — the sheer size of the companies created an illusion of being untouchable and unsinkable. Enron, Lehman Brothers, Blockbuster, Toys-R-Us, Borders, Myspace, Sears all went through the same process of blind belief in their own ability to withstand any storm or disruption.

Blockbuster, for example, at its peak in 2004, employed more than 60,000 people at its 9,000 stores. When Dish Network bought the bankrupt Blockbuster in 2011, it was staying afloat with only 1,700 stores remaining. But it did not have to go that way. Greg Sattel of Forbes explains:

“In 2000, Reed Hastings, the founder of a fledgling company called Netflix, flew to Dallas to propose a partnership to Blockbuster CEO John Antioco and his team. The idea was that Netflix would run Blockbuster’s brand online and Antioco’s firm would promote Netflix in its stores. Hastings got laughed out of the room. We all know what happened next.[vi] “

The Titanic Syndrome has sunk many companies. This is why it is time for us to meet this enemy. Titanic Syndrome: a corporate disease in which organizations facing disruption bring about their own downfall through arrogance, excessive attachment to past success, or an inability to recognize the new and emerging reality.

Why the Titanic Syndrome is More Dangerous to Business Today Than Ever

Once upon a time, our companies enjoyed long and healthy lives, with a slow rise to the top of financial performance and a gradual decline to annihilation. The rate of change was so slow that it was easy to develop the Titanic Syndrome and still survive -we had all the time in the world to renew our business on our terms. If a new “iceberg” showed up on the horizon — a competitor, a technology, a regulation — your company could adapt slowly and even get to enjoy the ride.

But that fairy tale is long gone.

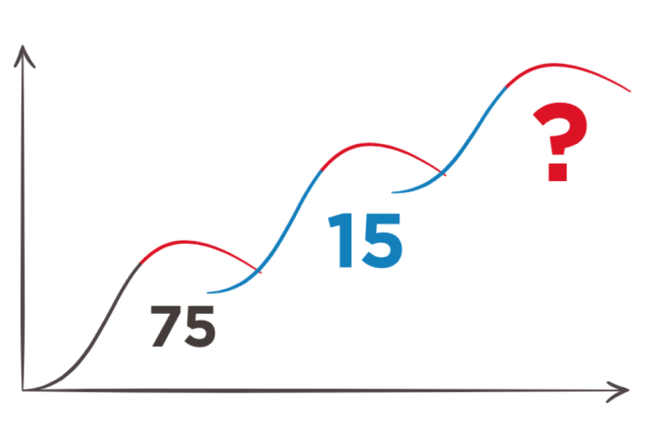

As Steve Denning of Forbes puts it: “Fifty years ago, ‘milking the cash cow’ could go on for many decades. What’s different today is that globalization and the shift in power in the marketplace from buyer to seller is dramatically shortening the life expectancy of firms that are merely milking their cash cows. Half a century ago, the life expectancy of a firm in the Fortune 500 was around 75 years. Now it’s less than 15 years and declining even further.[vii] “

Denning’s claims are supported by research published by Richard Foster and Sarah Kaplan in 2001[viii], which showcased how corporate life cycles were diminishing rapidly. Yet, much has happened since 2001.

The increasing level of globalization, showcased so painfully during the 2008–2009 global economic crisis, powered by the ever-increasing access to knowledge (think Google, free online courses, Khan Academy, etc), means that more of us are inventing every day and sharing those inventions globally. There is more startup activity today than in the past two decades[ix], threatening greater disruptions to existing business.

With all these pressures, the demand for corporate (economic, communal, and personal) reinvention has grown even further.

Does it mean that we are all doomed? Absolutely not. What separates companies that survive from those that go down is the ability to start a new lifecycle, to pivot their company far enough from the path of destruction to find a new opportunity for growth. But if before you had 30+ years to reach your prime, today you might only have a few years. How many exactly?

To answer this question, in 2018 we launched a global reinvention survey. More than 2,000 participants took part in this research giving much-needed insight into the speed of change and the ways to deal with it.

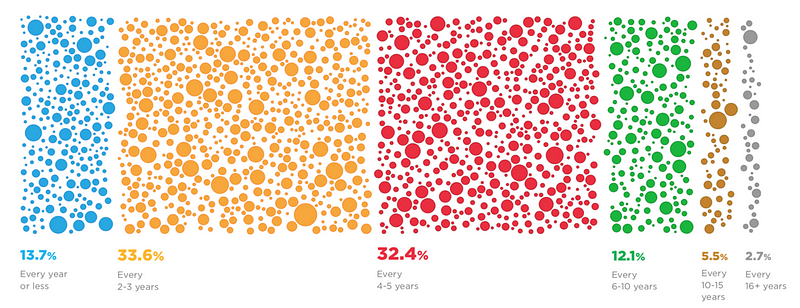

Research Insight #1: Reinvent Every 2–5 Year or Perish

The results of the study show that to survive today, most of us ( 0r 72.7%) need to reinvent every 2 to 5 years, with a whopping 13.7% reinventing every 12 months or less!

This means that barely into your existing business reality, you must start the reinvention process anew — again and again, in a continuous cycle of renewal. The business you are in today cannot be the business you’ll to be in 3 years from now. By then, you are either entering your new business or you are on the way to extinction. Period.

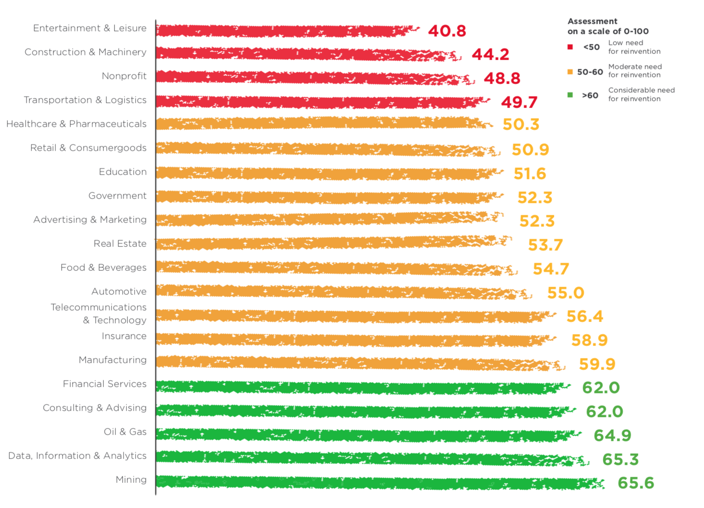

Research Insight #2: Not All Industries See Reinvention as a Priority

While some industries (for example, Retail, Consumer Goods, Financial Services, and Transportation) put a lot of attention on the need to renew and revive, others ignore threats of disruption. No wonder that Entertainment — the industry that reported the least interest in reinvention — is now a prime target for disruption by the start-up communities and big tech, with the most successful solutions coming from outsiders (think Netflex, Hulu, Amazon Prime):

Here is the scoop on this data: two scenarios matter for you.

- If your industry sees reinvention as a priority, but your company doesn’t, you’re at risk of losing to your existing competitors.

- If your industry sees reinvention as irrelevant, it is at risk of being taken over by start-up newcomers, but this offers a unique opportunity for your company to stand out.

Either way, it is time to face reality and start moving. Ride the waves of change, don’t get crushed by them.

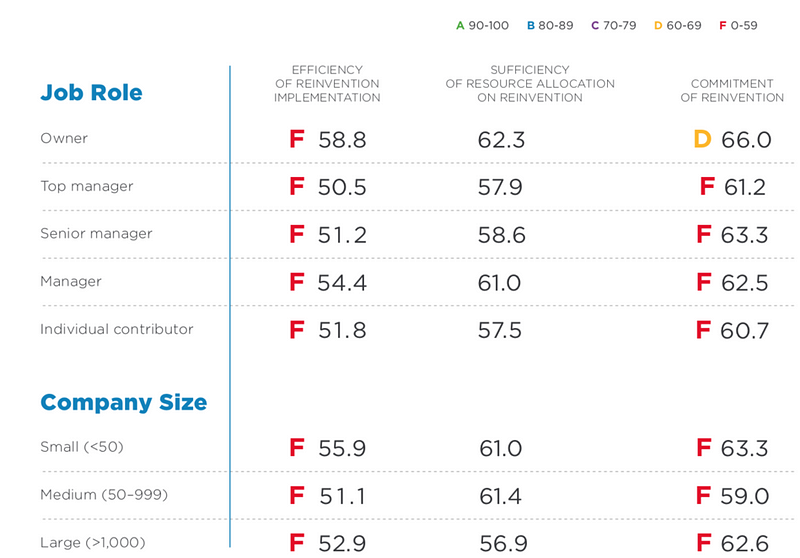

Research insight #3: Companies score a D in commitment and an F in implementation of reinvention

We asked companies to grade themselves on how committed they are to reinvention, how sufficient are resources allocated to continuous renewal, and how efficient they are when it comes to implementing change initiatives. They did so numerically, from a range of 0 to 100.

If we convert their answers to a standard grade scale used in most US schools, here’s what we discovered:

- When it comes to commitment, people give themselves and their company a grade of D.

- If that sounds bad, the grade they gave themselves for both the resources allocated to reinvention and the efficiency of their reinvention implementation is an F.

So, what can we learn from the Titanic Syndrome?

Titanic Syndrome is real — and so is the cure of reinvention. And here’s the deal: You don’t have a choice. Whether you like it or not, in the coming years you and your business will face more change, more disruption, than ever before.

The only choice you have is this: whether you will ignore change, whether you will disregard it in a desperate attempt to hold onto your past — or whether you will use change to turn it into your competitive advantage.

It’s simple.

About the author

Dr. Nadya Zhexembayeva is the author of the just-released “Titanic Syndrome: Why Companies Sink and How to Reinvent Your Way Out of Any Business Disaster”, published in December 2018 by Chief Reinvention Officer.

Dr. Nadya Zhexembayeva is a scientist, entrepreneur, and author specializing in resilience and reinvention. As a consultant, Nadya helped such companies as Coca-Cola, IBM, CISCO, L’Oreal Group, Danone, Kohler, Erste Bank, Henkel, Knauf Insulation, and Vienna Insurance Group reinvent their products, leadership practices and business models to meet new market demands and prepare for incoming disruptions. As a speaker, she delivered keynotes to more than 100,000 executives. As a business educator, she runs hundreds of Executive Education workshops for nearly 10,000 leaders. Nadya is the author of “Embedded Sustainability: The Next Big Competitive Advantage” (2011), named #38 on 100 Best Sustainability Books of All Time by BookAuthority, and “Overfished Ocean Strategy: Powering Up Innovation for a Resource-Deprived World” (2o14), SoundView Best Book of 2014.

[i] You can see this and many other details at “Titanic: 40 fascinating facts about the ship,” The Telegraph, April 11, 2017

[ii] This information comes from the transcription of the US Senate Inquiry, day 8. The full transcript can be found here: http://www.titanicinquiry.org/USInq/AmInq08EvansCF01.php

[iii] The role of the First Officer Murdock in the Titanic disaster can be further explored here: http://www.williammurdoch.net/man-07_decision_in_retrospect.html

[iv] You can read more about the story of this key in The Telegraph article by Graham Tibbetts titled “Key that could have saved the Titanic published August 29, 2007″

[v] Frederick Fleet testified before US Senate on this matter. The full transcript of the testimony can be found at: http://www.titanicinquiry.org/USInq2/AmInq04Fleet01.php

[vi] See more on this and other details of Blockbuster story at “A Look Back at Why Blockbuster Really Failed and Why It Didn’t Have To” by Greg Satell, Forbes, September 5, 2014

[vii] This quote comes from “Peggy Noonan On Steve Jobs and Why Big Companies Die” By Steve Denning, Forbes, November 19, 2011

[viii] See “Creative Destruction: Why Companies That Are Built to Last Underperform the Market-And How to Successfully Transform Them” (2001) by Richard Foster and Sarah Kaplan, published by Crown Business

[ix] See, for example, the Kauffman Startup Activity Index that shows the highest level of startup activity since 1998.

We think you might like this

#MemberSpotlight - Personal Branding: It's Not Enough to Just Do a Good Job Nowadays

Sandra Winkler

19 November, 2020

Oliver Aust, author and CEO of Eo Ipso, talked to us about personal branding, and why becoming unignorable is about helping others rather than promoting yourself.

20 Work Social Event Ideas for a Strong Company Culture

Mindspace

8 January, 2025

A strong company culture boosts employee morale, enhances productivity, and strengthens your brand, attracting top talent and clients alike. One of the easiest ways to foster this is through engaging social events. Looking for inspiration? Check out these 20 work social event ideas to elevate your team’s connection and energy.